DESCRIPTION

The insurance industry in many areas offers inexpensive insurance against damage by wind, and very expensive insurance against damage from flooding; FEMA offers inexpensive insurance against flood damage.

When a person purchases a home, the mortgage company invariably wants its investment covered by a homeowner’s policy – the typical homeowner’s policy includes insurance for damage done by wind, but, as the typical home is not imperiled by flooding, does not include insurance from damage due to flood waters.

Thus the problem faced by the inspector when a hurricane hits becomes: which was the damage caused by, the wind or the water. This course was created to help both those who are in that predicament due to the loss of their home or business, Insurance companies, and those who are providing assistance to the insurance companies.

PERFORMANCE OBJECTIVE

If the homeowner or business owner has wind damage insurance coverage but not flood damage insurance coverage (or coverage through another entity), the insurance company and the owner need to know the extent of the damage the wind is responsible for. This course will help the student recognize both wind and water damage.

INTRODUCTION

Wind:

The wind comes in two varieties, tornado and hurricane. In fact the two are many times called cyclones for their circular nature. Tornadic activity many times provides the higher winds (sometimes over 300 miles per hour), but usually in a smaller footprint (usually less than a mile across). Hurricanes generally have lower wind speeds (a Category Three hurricane has winds up to 130 miles per hour), but can cover a much greater area.

Resident: “There are many eyewitnesses to tornadoes in my area.” Typically what many eyewitnesses observe are water spouts. A waterspout is a non-supercell tornado over water. Waterspouts are common along the southeast U.S. coast and can happen over seas, storm surge areas, bays and lakes worldwide. Although waterspouts are always tornadoes by definition; they don’t officially count in tornado records unless they hit land. They are smaller and weaker than the most intense Great Plains tornadoes. They usually disperse immediately as they reach land and cause little damage. Other tornadic activity viewed might be short lived bursts called dust devils.

Water:

The water damage can be from the results of large amounts of rain, from the rise in the water from the ocean, or from failure of manmade structures. Hurricanes have dropped 12 inches of rain or more in a short time, and, which was the case with Katrina in 2005, can build up a 30 foot storm surge such as was experienced in Mississippi. The almost 16 foot surge in New Orleans overtopped one levee, undermined three other levees, eroded several levies, and came through openings not closed in several other locations. All of these cause flood damage.

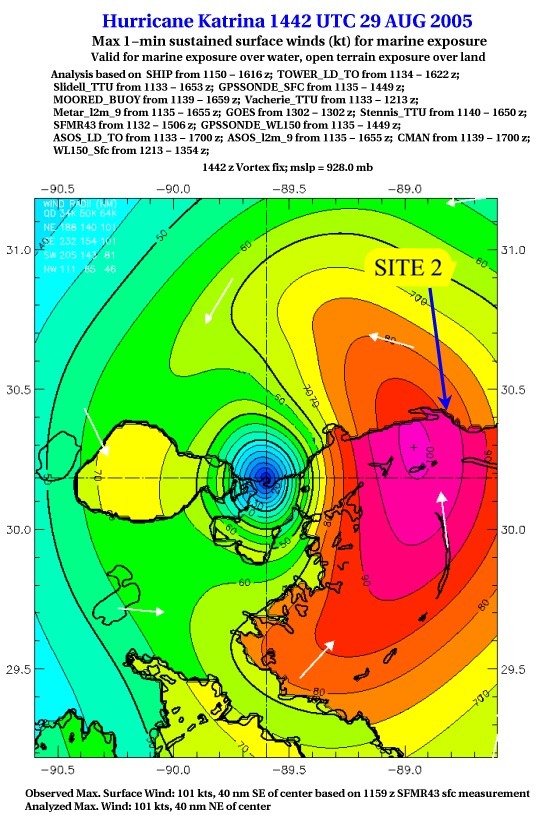

Below is a depiction of the winds from Hurricane Katrina:

The winds of Category 5 had subsided to that of a Category 4 as it hit the tip of Louisiana, and diminished to that of a Category 3 hurricane as it came ashore in Mississippi.

Below is a snapshot of the wind intensity (new Orleans is in the green and blue area on the left above the lake, to the left of the ‘60’):

Below is a snapshot of the surge, the x shows the center of the hurricane, New Orleans is on the extreme left:

You may notice that the worst surge is 30 feet in Mississippi, the red area to the right of the storm center. Islands which were inhabited were well under water and invisible during the storm.

The weather service provides much of the data which can be used to determine what happened in the area in question:

FEMA – BATON ROUGE, La. –

To receive appropriate financial coverage for water damage sustained from Hurricanes, the definition of the type of damage is necessary. The U.S. Department of Homeland Security’s Federal Emergency Management Agency (FEMA) is offering the following guidelines to better understand flood and wind-driven rain damage.

The simple definition of a flood is an excess of water on land that is normally dry. The National Flood Insurance Program includes in their definition inland tidal waters; unusual and rapid accumulation or runoff of surface waters from any source; collapse or subsidence of land along the shore of a lake or similar body of water as a result of erosion or undermining caused by waves or currents of water exceeding anticipated cyclical levels that result in a flood.

Homeowner, renter and business owner insurance policies DO NOT cover flooding. Generally, policies will cover wind, rain, hail, wind-driven rain, and lightning damage. A separate flood insurance policy is needed to protect homes, businesses and personal property against flood damage. If a home, business or other residence is in a FEMA-identified high risk flood zone, a separate flood insurance policy should have been required on a mortgage transaction.

Rain or wind-driven rain, and hail damage are not in the same damage category as floods. Wind-driven rain damage, regardless of the cause, is a covered peril like wind or lightning which may have caused an opening in which rain has entered and caused water damage to the home or personal property.

Hurricane Katrina accounted for some $63 billion in insured losses, with $45.1 billion from wind losses and $17.7 billion from flood damage, most of which were incurred in Louisiana and Mississippi.

The Broussards sued State Farm for refusing to pay for any damage to their home, which Katrina reduced to a slab. The couple, who wanted State Farm to pay for the full insured value of their home plus $5 million in punitive damages, claimed that a tornado during the hurricane destroyed their home. State Farm blamed all the damage on Katrina’s storm surge.

In order to get the foundation scrubbed clean like the Broussards’ requires a massive surge of water. It may be possible with sufficiently strong, sufficiently sustained winds, but much more powerful storms than Katrina have failed to produce that sort of result. Katrina wasn’t even a particularly powerful hurricane when it hit land.

Judge Senter, however, ruled that State Farm couldn’t prove that Katrina’s storm surge was responsible for all of the damage to the Broussards’ home. The judge also said the testimony failed to establish how much damage was caused by wind and how much resulted from storm surge.

In this course we will try to work through how to establish those damages.

BODY

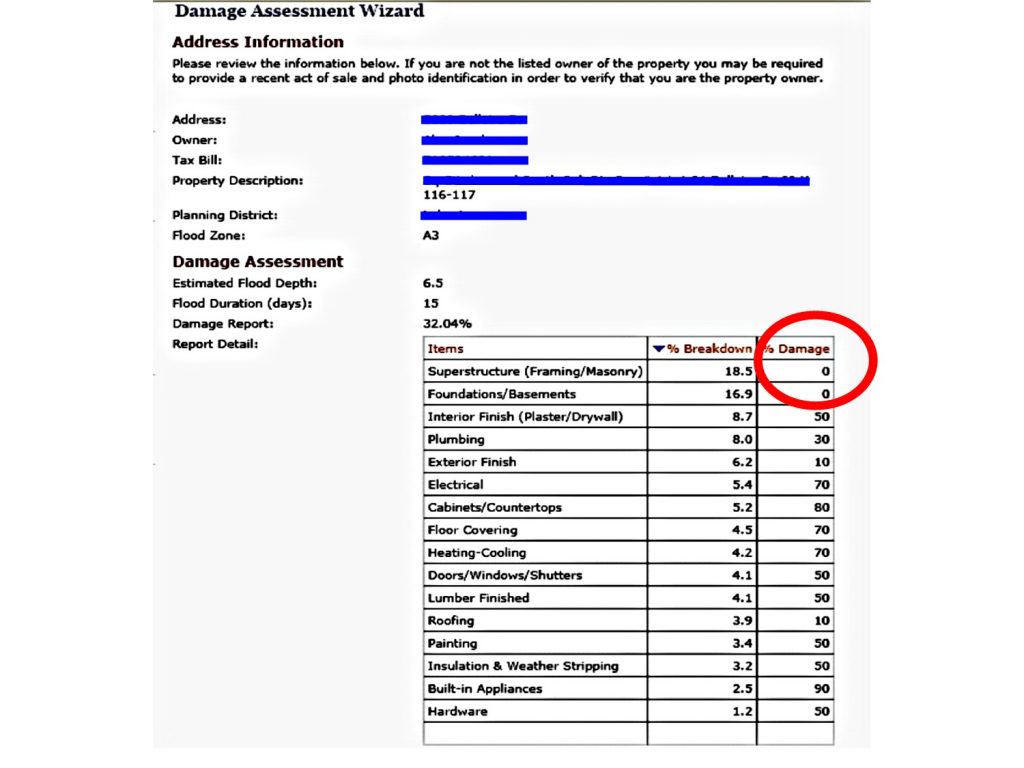

A consulting engineer (A) was asked to write a report relative to damage due to wind vs. water for the following site. In the report the engineer (A) stated that all of the damage was from wind. As you can see from the first photograph below, the home was not damaged at all on the outside, the rood and shutters were intact.

The second photograph (below) shows that the water reached almost to the top of the side door. One can also see that the water was not affected by winds as the debris line (wrack line) was quite level.

The owner had hired a contractor who removed all of the water damaged wall board and treated the studs with bleach.

The water did not reach the second floor, but the owner had the contractor remove the carpeting to avoid mildew in the carpet:

The wall covering and ceilings on the second floor were in perfect condition:

The engineer (A)’s report stated the following relative to the winds from Katrina:

• “The stress points on the building are related to a hurricane wind impact demonstrated in the building movement and twisting.”

• “The stress points exhibited at the house structure indicate that the superstructure suffered from the force of the wind impact at an early stage of the storm.”

• “The stress points are mainly found at the interior fenestration framing such as doors and windows.”

• “The cracks were noticeable almost at all window frames at the connecting points and at the front door. These are new and small in nature.”

• “The house and the structure was affected by the hurricane winds, then later on by the flooding from a sustained saline water for several weeks and finally by the prolonged wet/dry condition causing further structural damages by thermal expansion and creation of the stress points after the flood water receded.”

He went on to say that there were “no broken windows”, the “second floor is intact”, ”The second floor sheet rock did not show visible cracks”, “The brick siding sustained well the impact and no substantial cracking was found”. and “wet/dry expansion causing cracking at the door and window frames.”

The author’s response was as follows:

The author disagrees. Katrina’s less than hurricane force winds (60 miles per hour max at this location) did not move or twist the building or cause any “stress points” – there was no evidence of any movement or twisting found during our investigation.

If the building had “twisted”, the windows would have broken, the plaster and sheetrock walls and ceilings would have cracked and the brick veneer would have cracked. Thus there is no evidence of any movement or twisting.

Furthermore the engineer states “structural damages by thermal expansion and creation of the stress points after the flood water receded.”. thus any “stress cracks” the engineer found he says were not caused by the wind but by “thermal expansion”- after the water receded. The engineer also states “and wet/dry expansion causing cracking at the door and window frames.” and “The cracks .. are new and small in nature.” Thus they could not have been caused by the hurricane winds, nor were they visible to the naked eye. It is unclear to author as to the basis for the contradicting conclusions of the engineer.

The engineer in question must have brought along a microscope because there were no cracks visible. A common thread amongst the homeowners is the battle cry “My house was twisted by the wind.” Someone must have started that refrain and it has resonated throughout the Gulf Coast. The author has yet to see a house “twisted” in my more than 200 inspections. In all cases, either the house had real damage caused by the wind, was swept away by the storm surge, or was in good shape. Using big words such as fenestration, stress points, and superstructure do not help prove any point, but are included to mask a poor report.

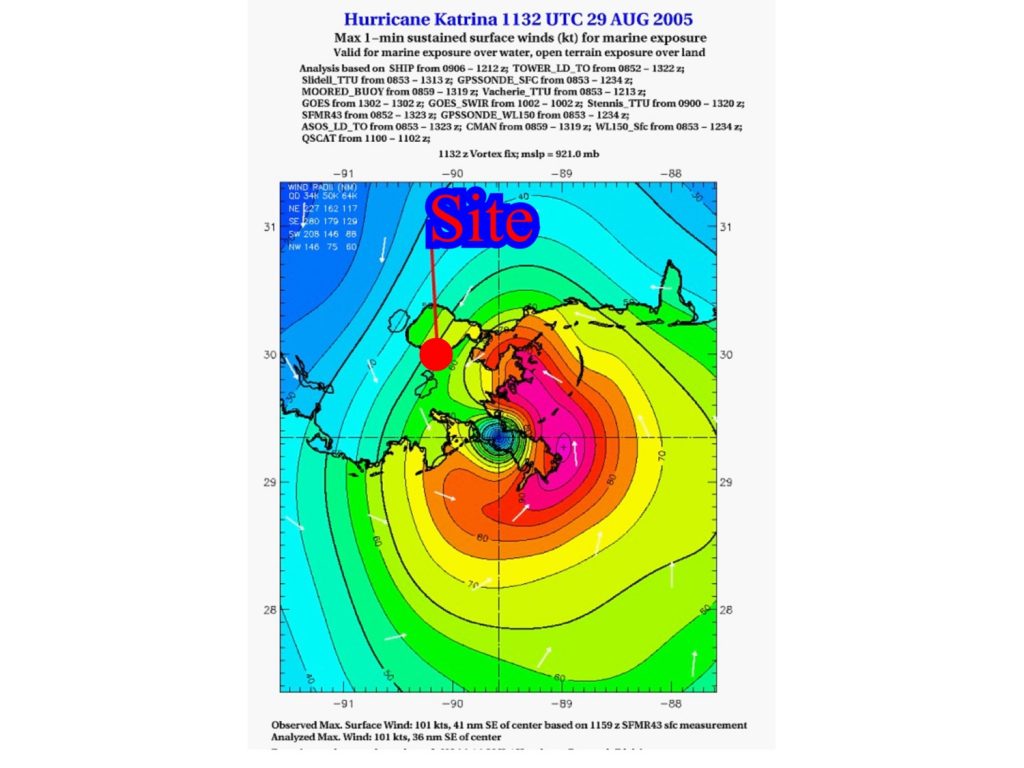

Below is the location of this site, well away from the high winds (in pink) from the hurricane:

In addition to the inspection was the municipality’s report which indicates no damage to the superstructure or foundation:

Hurricane Katrina did not produce much in the way of hurricane strength winds in the residential New Orleans area, and no tornadoes in Louisiana at all. The homeowners for the most part (60% of affected homes) did not have flood insurance, but they mainly did have insurance for wind damage. Therefore, at most of the inspections the author conducted, the homeowners were hoping that we could find something wrong that the wind had caused so they could get something (i.e. more than nothing) for their destroyed home that the day before was worth from a quarter million to four million dollars.

CONCLUSION

In this first scenario it was quite obvious that the engineer (A) hired by the homeowner was trying hard to create a doubt that all the damage was done by water. He had no pictures that showed cracks, and no evidence at all that wind did anything. Most homes are designed to withstand winds of 60 miles per hour with little or no damage, but no home is designed to withstand water up to the top of the first floor doors.

Claim: Wind Damage 100%; Water Damage 0%

Result: Wind Damage 0%; Rising Water Damage 100%

SCENARIO TWO

In this second scenario, the wind and the water have played a role. The location is a home in Mississippi. The wind was over 115 miles per hour (Category 3) as the storm came ashore. Subsequently a 22 foot storm surge came to this location. The homeowner claimed that no surge occurred, all the damage had been done by the wind. Luckily there were remains to provide evidence.

After reviewing all of the evidence, my conclusion was:

- The residence was not damaged by wind with the exception of 200 square feet of roof covering that was damaged (roofing tabs were missing) and 10 square feet of soffit that was displaced.

- The remaining observed damage to the residence was the result of the storm surge from Hurricane Katrina.

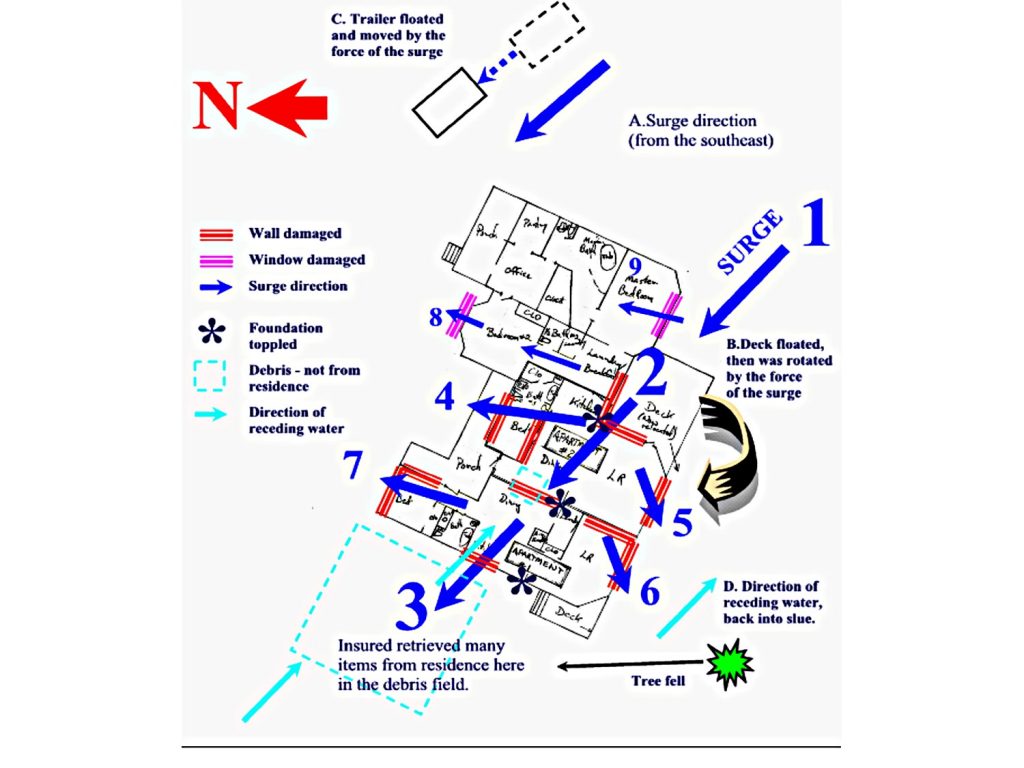

- The structural integrity of the residence has been compromised by the storm surge from Hurricane Katrina as shown in the following sketch:

The surge entered the structure at #2, then pushed out walls and windows at #3, #4, #5, #6, #7, and #8!

Below is the wind diagram for the area:

This structure was in the red area on the above wind map and experienced the brunt of the storm winds, and surge about an hour later. When the surge came, the hurricane’s eye was north of the structure, thus the winds had subsided somewhat, but up came the water. The structure was up on a 15 foot hill and thus only had six feet of water inside.

The following pictures were taken 35 days after Hurricane Katrina

The first photograph shows, on the left, where water pushed the wall in: conversely, on the right is where the water pushed the wall out (it is laying on the ground in pieces)! The author was standing at point #6, the wall that was between #5 and #6 was gone except for the studs and the molding along the base.

Below, the roof shingles on the south side of the structure were blown off by the wind. Note the trees that took the brunt of the wind.

The home was floated by the water, the foundation pilasters fell over, and when the building came back down, it fell where much of the foundation had failed. The plumbing stack had no place to go, so it pushed right up through the roof as the building fell off the foundation:

The above photographs really prove that the wind did very little damage – the roof and vents are still intact.

This home survived the Category 3 winds, but the storm surge came knocking, and then came right in:

Note that the venetian blinds were not disturbed (and turned into artwork). If wind had opened that door, the blinds would have been a mess.

WATER SURGE FROM A HURRICANE

The water comes in smaller waves, not in one huge crashing wave like tsunami. As one survivor explained to me, “There would be a lot of small waves, then a big wave would come, but not go out. Then a lot of small ones, and another big one, “banging the building”, that did not go away. When one very big one came, I jumped out my second story window in time to see my building cave in from a huge wave. If I had not jumped, I would have been trapped inside. I hung onto the top of a tree and watched seven bodies float by as the water receded – I could not help them.” Thus the surge came up incrementally, finally building up to 30 feet. As the water moved in, it floated buildings, broke down walls, and generally destroyed everything in its path. It then went down as slowly as it had arrived. A separate course on RedVector quantifies the forces of the advancing surge.

WRACK LINES

The wrack lines in one structure the author observed prove that a floating object cannot be used to gage water depth or status of the wind or water at any given time. One engineer used a sloped wrack line on a floated couch as “proof” that a structure had been blown down by the wind prior to the flood. The floating material in many structures that the author has seen showed that furniture – in a room that was protected from the wind (interior with no broken windows or open doors) – can have many wrack lines. If a house floated (and many did) a house also can have more than one wrack line, no matter whether there was wind or not.

One home that had floated across the road had two wrack lines, one on the high side and one on the low side as it floated along. The homeowner had put a “miracle” article in the newspaper, relating as how her home had been picked up by a tornado, then put back down on the other side of the road without disturbing anything inside! She had tried to clean up all the signs of water inside the home but left a couple. The author removed a plywood panel and found the wrack line 18” above the floor on the rear of the house and found the wrack line in a front closet 9” above the floor. Underneath the structure were piles of marsh grass that had been affixed to the underside as it floated along. So much for a miracle!

DEBRIS

It is difficult sometimes to find parts of the structure in question, especially if the structures in the direction of the flood have been demolished and their debris is in your parking lot or yard, carried there by the storm surge. If wind had moved the debris, there would have been much more small impact damage to the walls, and the windows most likely have been broken. The trees would have been damaged more than they were. In addition, the chain link fences would not have held back the floating debris as it did in many cases.

ROOF SHINGLES AND TILES

In general, roof tiles were removed from the south and east roofs, the direction of the advancing storm, the north and west roof shingles (and covering) were not affected. In the time lapsed since most of the buildings affected by Katrina were roofed, the adhesive on roof shingles has changed. The newer (post 2005) shingles do not come off so easily

Things to check for:

1. Broken windows.

2. Broken tree branches (or lack thereof).

3. Wrack lines (highest line debris collected) inside, and outside. You may have to look inside of closets, between the front door and a storm door, or any enclosed space to find a line.

4. Path of debris.

5. Roof covering damage (or lack thereof).

6. Gutters and shutters.

7. Debris under structures.

8. Neighboring structures (were they at a higher elevation and thus did not get destroyed by water?).

9. Bark rubbed off of trees (debris in the water will rub the bark off many trees).

SCENARIO THREE

This mansion was submerged in water to 5 feet 3 inches above the floor. Investigation also found damage due to wind.

In the rear everything looks fine, but if you look closely, the bicycle is quite rusted. The pool has been emptied, the debris and foul water cleaned out and the pool was refilled.

One culprit, a loose piece of flashing and a failure to seal the enclosure. Under this spot we found that the ceiling had leaked into the enclosed area, destroying the floor covering.

Note the plastic over the wind turban stack. The wind turbines are usually the first to go, a tip off of some high winds.

3-5

The high water mark was quite visible on the glass going up the steps. It measured 5 feet 3 inches. Water destroyed all of the wall board on the first level, as well as all the furniture and appliances.

The wall board all had to come off, and the fireplace was being replaced. The electrical wiring had not been replaced – the wiring is not required to be replaced unless the ends are corroded. A resistance test on all wires to be left in place is needed to insure that they have not been compromised – if it were mine, the cost of new electric wires would bring peace of mind, if nothing else.

The ceilings were not affected, this hardwood ceiling was able to be kept.

The gym walls and ceiling on the north side were not affected but the floor covering had been removed due to the leak on the south side.

This is the leak location on the south side of the gym, water was still dripping from the ceiling,

My initial thought was that the sauna water heater in the attic may have been leaking, but it was not near the leak, nor could the author find any evidence at the heater of any leaks.

In any event, all facets of the structure need to be investigated. The author did not have his infra red camera with him, or the source of the leak could have been traced better.

Is the claim reasonable? In this case the Claim: Wind 10%, Water 90%. Wind damage many times will occur prior to a structure being inundated and possibly destroyed. Roof shingles will come off, roof turbines will be blown off, leaks will occur and the interior will be damaged. Allowing for 10% of the value of the residence to be used as damage is prudent in many cases where there had been high winds. Even though the structure may no longer exist.

SCENARIO FOUR

Below are a series of pictures taken in the flooded areas. Not much question of wind on some, but others?

The house below is where a gentleman and his 80 year old mother stayed to ride out the storm. The top right window is where they climbed out into a boat. “My mother refused to leave before the storm, so I stayed with her. After two days without water or food after the storm, I swam down stairs and maneuvered the floating refrigerator so that I could open it and get whatever was still edible out for us to survive on. After four days a boat came and rescued us, but my dog could not fit in the boat. By the time I was able to get back he had lost 30 pounds, but he was OK.” Wind 5%, water 95%; confirmed.

A typical car after the water subsided. The only thing of value in a car after being submerged in salt water for weeks? The lead plates in the battery. Wind 0%

This home (below) floated, it originally was supported by the red brick posts until 8 feet of water covered the area. Claim: Wind 100%, water 0%; after inspection Wind damage 10%, water damage 90% (roof vent still in place, but some roof covering damage).

Ten feet of water covered this area. The mobile home that occupied this spot was never found. Some engineers the author know would give the homeowner 100% wind, but as the wind in this area was only 45 miles per hour, the author say 10% wind, 90% water. The home most likely floated off across the miles of grass beds (past the trees).

Typical living room, the ceiling has collapsed due to water being 9 feet deep here. The roof was intact, thus 100% water.

According to this homeowner, the concrete floor cracked because of the hurricane. “It was not like this before the hurricane – the wind shook the house and cracked my kitchen floor. I had to put something into the crack because ants were coming in.” As the house was built on soft clay that was subsiding all around, and the fact that she was 100 miles from the hurricane.. 0% wind.

“The wind did all of this damage!”

Just because the water was 5 feet deep did not mean anything?

The lady’s husband was a doctor. Now his practice was gone, their home was destroyed, and they had no flood insurance. Now they have to start over with nothing.

Mold starts to grow quickly in some flooded rooms:

“Wind made the second floor lean.”

Lady, those termites having eaten all the way through the supports did have something to do with it.

Termites 1 – Wind 0

“My kitchen floor did not lean like this before the storm! The wind pushed my house and racked it.”

There was no flooding in this area, neither was there any wind.

Her husband had tried to level the house 10 years ago she said.

Result: Wind 0%, Structural failure 100%

SCENARIO FOUR

FALSE ADVERTISING

Below is a picture taken during the storm. Note the yellow pole in the bottom left. This picture was labeled as if it was taken in downtown New Orleans where people were angry about a canal.

This is the actual location of the picture (looking in the reverse direction)- it was taken from a window in the industrial building in the background, the yellow pole is in the bottom middle (at the end of the dumpster). THE AUTHOR took this picture after the storm. This just goes to show to what extent some people will go to try to inflame others to their point of view.

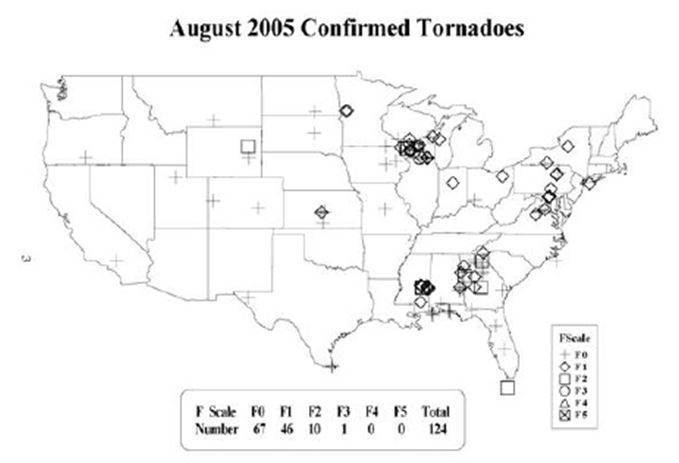

TORNADOES

Many people claimed that tornadoes hit their homes. Below is the official map:

There were no tornadoes in Louisiana at all! The news media showed tornado warnings, but that is because hurricanes many times do spawn tornadoes. Katrina was moving fast and did not spawn any to the west side of the storm. If damage was by tornado, then the homeowners insurance would pay, thus many homes destroyed by water were claimed to be hit by a tornado.

Below is a picture of damage by a real tornado. The 2X10’s were securely fastened to the structure, and the roofing was securely fastened to the 2X10’s. The tornado split the 2X10’s down the middle, taking the roofing with it!

LONG BEACH

The author’s first inspection was in Long Beach. The homes were leveled there. A typical 16,000 square foot building was reduced to a slab, a screwdriver, a door knob, and a handful of change. 28 kids decided to stay in one of the buildings where they decided to have a Hurricane Party. The building is now gone, and so are the kids.

There was an article in a trade magazine recently that was very alarming, it read in part:

“The client was battling against an insurance company that denied his claim, citing that his home was damaged by flooding and not wind. His effort to retain other engineers in the Southeast proved fruitless. Engineer (B) saw firsthand the reason for his client’s frustrations when he traveled to the area. Houses in the Long Beach, Mississippi community had only their foundations or front steps left; nothing else remained. Plastic bags and clothes littered trees nearly 30 feet high. Refrigerators, cars, and timber were pushed into piles by the storm surge. “People were picking through the piles, trying to find personal items, it was a heart-wrenching and devastating scene.”

With a 35-page report backed up with 200 pages of supporting materials, Engineer (B) offered information to prove that the home was destroyed by the wind. “The basic premise was that if there’s no house, there’s no evidence,” he says. “After four or five hours on site and more than 350 photographs, I was able to analyze everything and conduct research within a couple of months.” The client received 100%of his policy benefits.There are other homeowners dealing with the same predicament, and Engineer (B) has offered his forensics expertise.” The author asked Engineer (B) about his report wherein he had testified that wind entirely destroyed the structures in Long Beach, and that water did no damage. He confirmed that, and said that “the opposing engineer had some “silly formula” that showed where water was moving at a certain speed and knocked the walls down, but that was ridiculous, the wind was blowing at 130 miles per hour – that destroyed all of the buildings…. the water only came to elevation 27 feet … testimony from witnesses (residents) and videotapes from a TV crew showed that the wind did all of the damage.” He was glad that “some of us have integrity and will tell the truth, where others do not.” The author asked him where he had found his evidence – he promised to send some links for web sites (never received). The author asked to see a copy of his report, but he said it was still in litigation and not available (disproving that the client got the claim paid?). He said that he had been to a conference on Katrina in January and was pleased to find that “everyone there agreed with him that wind had done all of the damage due to Katrina”.

Below is the actual data, the wind did not reach 130 miles per hour in Long Beach, it did not even reach Category 3 status. The wind was only about 100 miles per hour as Katrina came ashore in accordance with this graph. The storm surge was measured by the author to be 30 feet above mean sea level. Winds of 100 miles an hour will not destroy well built buildings, but an advancing storm surge will.

Above the graph shows that winds come before the surge, and have diminished somewhat by the time the surge peaks.

Below is that referenced “silly” formula. It looks complicated, but it is not. As indicated, the pressure of 5 feet of water on a wall is 40 times that of a 120 mile per hour wind. A well built structure can handle 32 pounds per square foot of pressure from a 120 mile per hour wind, but certainly cannot survive 1280 pounds per square foot of water pressure, as the survivors attest. Only those who are tempted by insurance money can ignore the facts:

Below is the applicable storm designation: a 100 mile per hour wind relates to a mid Category 2 Hurricane and will not leave just a slab behind.

The items needed to be observed to determine damage from wind are: damage to doors, windows, roofs, nearby mobile homes, and trees.

Interview with Senator Trent Lott:

“MATTHEWS: Can you get your house rebuilt? Are you going to get—you‘re insured and all that? Or how does it stand?

LOTT: Well, I did have flood insurance and I have collected flood insurance. But it‘s not enough to pay for the cost of our losses, of course.

And I had a household policy that covered wind, but I‘ve been told so far by my insurance company that I didn‘t have any wind damage, that‘s not credible or believable.

So on our behalf, on a personal basis, but on behalf of a lot of other people—probably 100,000 people situated similarly to us—I am aggressively pursuing, you know, some additional recovery so we can afford to build a house.”

The results of that determination that there was no wind damage was interesting:

Lott had hired Scruggs who, in addition to Lott’s lawsuit, also created a Scruggs Katrina Group to pursue similar lawsuits…

Lott, meanwhile, declared war not only on State Farm … but on the entire insurance industry. He introduced legislation requiring homeowner insurers to clarify what their policies cover and what they don’t; he co-sponsored legislation to eliminate the antitrust exemption for insurance companies; he brought Hood up to Washington to testify before the Senate commerce committee, of which he is a member; and he entered internal State Farm e-mails concerning Katrina coverage into the Senate hearing record.

According to Chuck Chamness, CEO of the National Association of Mutual Insurance Companies, Lott phoned him last year and threatened “bringing down State Farm and the industry.” It was, complained Wall Street Journal editorialist Kimberley Strassel, “a ferocious campaign of political revenge that would make even Henry Waxman envious.” Strassel even called it “extortion,” noting that State Farm had quickly settled with Hood and Scruggs, and paid off Lott. (The settlement has since come unglued.)

Lott, who in the past has publicly called for limits on lawsuits, as noted, has sponsored legislation after Katrina that would end the insurance industry’s exemption from antitrust laws (thus removing any limits!).

The insurance companies also have an interesting time with determining wind vs water:

The Branch Consultants are a group of former insurance adjusters who documented what they say is a pattern of insurance companies systematically shifting hurricane damage bills that private companies should be paying through homeowners insurance policies onto taxpayers across the country through the National Flood Insurance Program. To prove their point, they collected insurance adjustments by different companies for flood damage and wind damage, then went back to the homes to readjust the claims. They found homes with no evidence of flood damage that had been paid for flood damage, and documented 57 cases in their lawsuit where people where overpaid on flood damage and underpaid on wind damage.

The Rigsby suit was brought by two sisters from Ocean Springs, Miss., who worked for E.A. Renfroe Inc., an Alabama adjusting firm that worked for State Farm. They bolted with copies of 1,500 pages of claims documents and allege that insurance companies manufactured engineering reports to falsely deny insurance claims and shredded documents that were unfavorable to them.

So, how does one prove wind or water for a slab? There is no real way. With no evidence you cannot “prove” anything, you can only use parochial evidence to give the best answer available.

Tornadic activity is described as follows:

You may note that if wind caused damage severe enough to level a home, the damage surrounding the structure would also be severe. If the surrounding vegetation is intact, and the displaced material is local, the wind may not have caused the destruction.

In the photo below, the water in this area was 12 feet deep during the surge. The owner claimed wind damage 100% for the slab in the foreground.

The evidence? The author checked the surrounding area. The refrigerator from the kitchen in the house next door to the left was found having floated up into the attic of the house. It had broken a wood member and ended suspended there in the attic. No wind the author knows of would have propelled a refrigerator from the kitchen into the attic. The trees were all dead from the salt water, but not shredded by the wind. The lower portions of all four sides of the neighbor’s roof were damaged, but not from wind, from water. The top of all the roofs in the area were intact, the walls were pushed out as shown by the yellow arrow by the receding water. Tire tracks imply that the building was leveled by machinery, not the storm!

A consultant’s tornadic activity report concluded as follows:

My conclusion: Wind 20%, Water 80%

Data may be found using National Weather Service (National Oceanic and Atmospheric Administration) available on the Internet:

The below , a missing trailer was also a 100% wind claim that had experienced the winds as shown above:

Yes, there had been a trailer here, but what about the building to the left, and the roof to the right? If the wind had been strong enough to take the trailer away, it would have taken the roof too! The water in this area was 5 feet deep during the surge. The wind was less than 50 mph. My initial thought was that the trailer most likely floated away, however in discussing the situation with the neighbors, it was discovered that the owner had taken the mobile home away!

Conclusion: Wind 0%, Water 100% damage…( Owner 100% removal!)

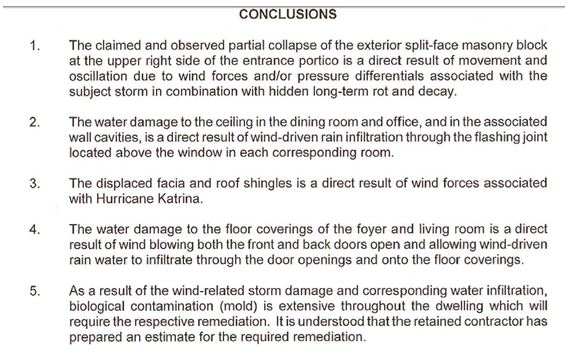

Below are the conclusions reached by engineer (D) for a house which was claimed to be 100% damaged by wind and was abandoned due to extensive mold:

Now we have oscillation of structures claimed! My investigation shortly after the storm found some interesting things:

There was no obvious damage to the floor coverings. There was extensive mold in the vicinity of the leak however:

The owner claimed 100% wind damage, my findings were 100% poor construction!

SUMMARY

There is no “foolproof” way to different differentiate between wind and water damage when all you have left is a slab. One can however find many clues from the surrounding areas. Wind will shred a building, dropping pieces for miles: a storm surge will bulldoze it down, leaving a pile of debris at the wrack line. Wind will severely damage the adjacent trees. The tree across the street from where one tornado hit was twisted off in the middle, the entire top 40 feet of the 18 inch pine tree was not found! Wind will drive debris which will break windows nearby. Water will demolish homes for miles based upon the terrain; tornados will take out individual homes away from the water as well as on the water. Building a case for wind vs water will take work well beyond the property in question, as well as data from many sources.

Things to check for:

1. Broken windows (especially up high where wind propels debris).

2. Broken tree branches (or lack thereof).

3. Wrack lines (highest line debris collected) inside, and outside. You may have to look inside of closets, between the front door and a storm door, or any enclosed space to find a line. The local wrack line for the flooding is also important.

4. Path of debris, and amount delivered where. Wind will drop debris for a long way, floating debris usually will be local.

5. Roof covering damage (or lack thereof).

6. Gutters and shutter damage.

7. Debris under structures.

8. Neighboring structures (were they at a higher elevation and thus did not get destroyed by water?).

9. Bark rubbed off of trees (debris in the water will rub the bark off many trees).

Weather reports from many sources should be consulted to bolster your findings.

CONCLUSION

Parole evidence is your best way to prove your case. Evidence of a wrack line where the client says no water existed is quite convincing. Swamp grass affixed to the underside of a house where the client says a tornado lifted the house. Adjacent trees, roofs, buildings not damaged by wind, but surrounded by buildings which had been submerged in water. Weather reports need to be obtained. National firms can create detailed, site specific reports. These are all prime examples of data needed to be collected. The case will never be “air tight”, but the more evidence, the better your decision can be upheld.